Whakarāpopototaka mākete / Market Commentary

Market Summary

This market update is for the three months to 31 March 2026.

With a new Middle East conflict continuing Iran effectively closed the Strait of Hormuz, where roughly 20-25% of the world’s seaborne oil trade flows through. This drove a large spike in crude oil prices, with prices nearly doubling over the month as the number of oil tankers transiting the strait fell to near zero. Central Banks had a generally muted response to this though as the US Federal Reserve kept interest rates unchanged and the European Central Bank, Bank of England, and Bank of Japan all coming to the same conclusion.

In New Zealand the RBNZ indicated that they would be waiting to see the downstream impacts of the Middle Eastern conflict show up in economic data and inflation readings, before assessing their next move for interest rates.

NZ GDP for Q4 2025 was released and weaker than expected (+0.2% q/q), although consistent with the view that the NZ economy is currently in a “recovery” phase. Overseas shares fell -5.7% (MSCI World – local currency) in March, driven by geopolitical tensions, higher oil prices and expectations of interest rate rises to deal with higher inflation.

New Zealand equities fell -5.8% in March, with global market forces proving a headwind for domestic markets. New Zealand’s reliance on fuel imports and relative distance from fuel exporters created supply strain over the month, which in turn led to higher fuel prices and pressure on business margins.

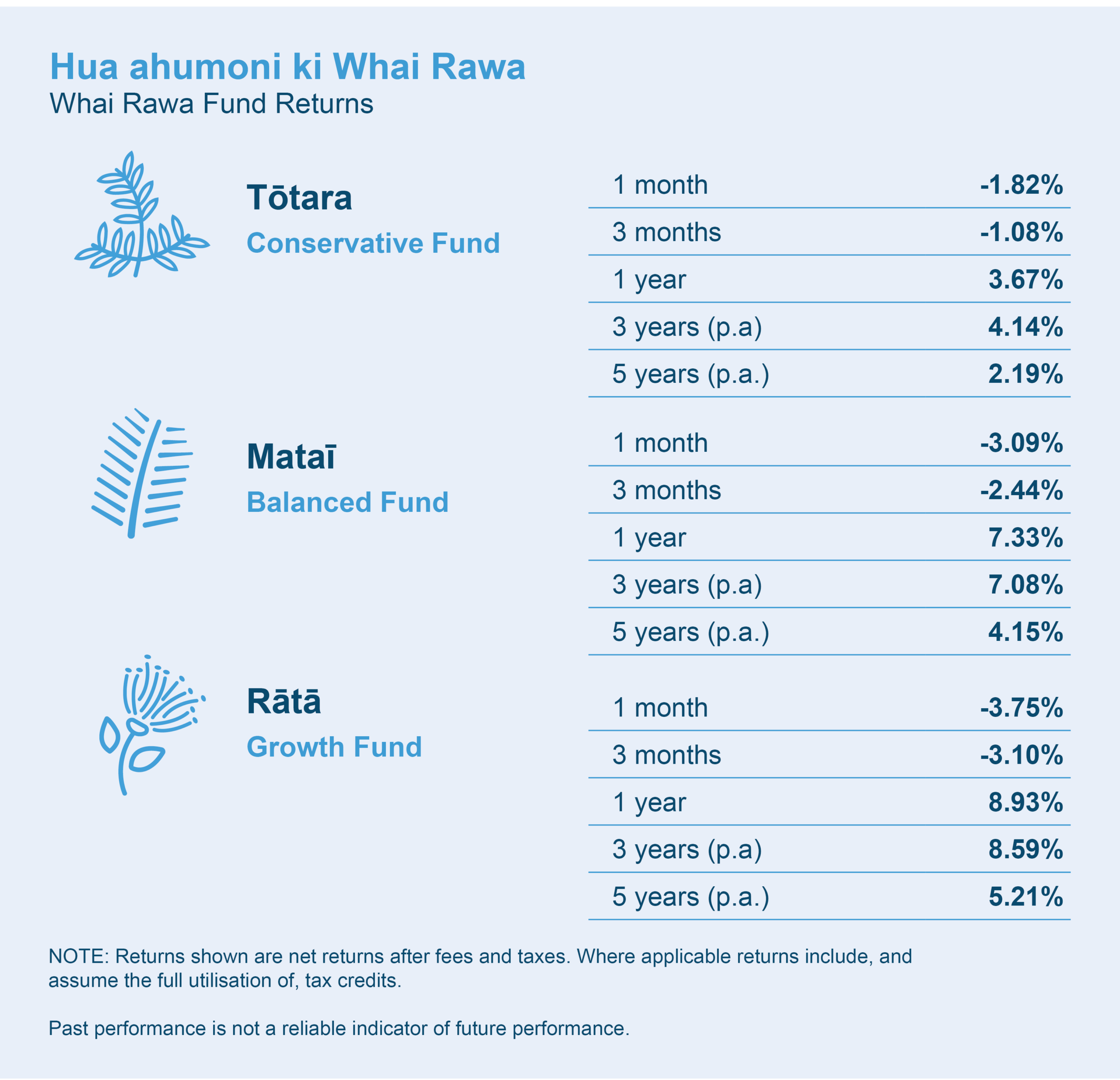

All three Whai Rawa funds had negative returns for the quarter to 31 March 2026.

For the quarter our Tōtara-Conservative Fund returned -1.08%, our Mataī-Balanced Fund returned -2.44% and the Rātā-Growth Fund returned -3.10%. These returns are after fees and taxes (at a 28% prescribed investor rate or PIR).

How does this affect my Whai Rawa account?

It’s important that with any investment you are prepared for ups and downs in your balance and that the fund you choose fits with your risk profile and timeframe for investing. A negative return is definitely unsettling, but market volatility and short-term swings are a normal part of investing. Your investment is designed for the long term, and ups and downs through these periods over time is expected.

How do I know if I’m in the right fund for me?

Take our 5-question risk quiz on our website to ensure your fund choice and risk profile match. Head to www.whairawa.com/riskquiz.